A Step-by-Step Guide to Zero-Based Budgeting

You check your bank account mid-month and wonder where all your money went. Payday is still a week away, and you’re trying to avoid dipping into savings or using a credit card to pay for gas and groceries. Sound familiar? You’re not alone in this financial mystery.

Millions of Americans feel like their money disappears before they can make real progress on their goals. The good news is there’s a simple solution that can help you regain control of your money. It’s called zero-based budgeting, and it might just change your financial life forever.

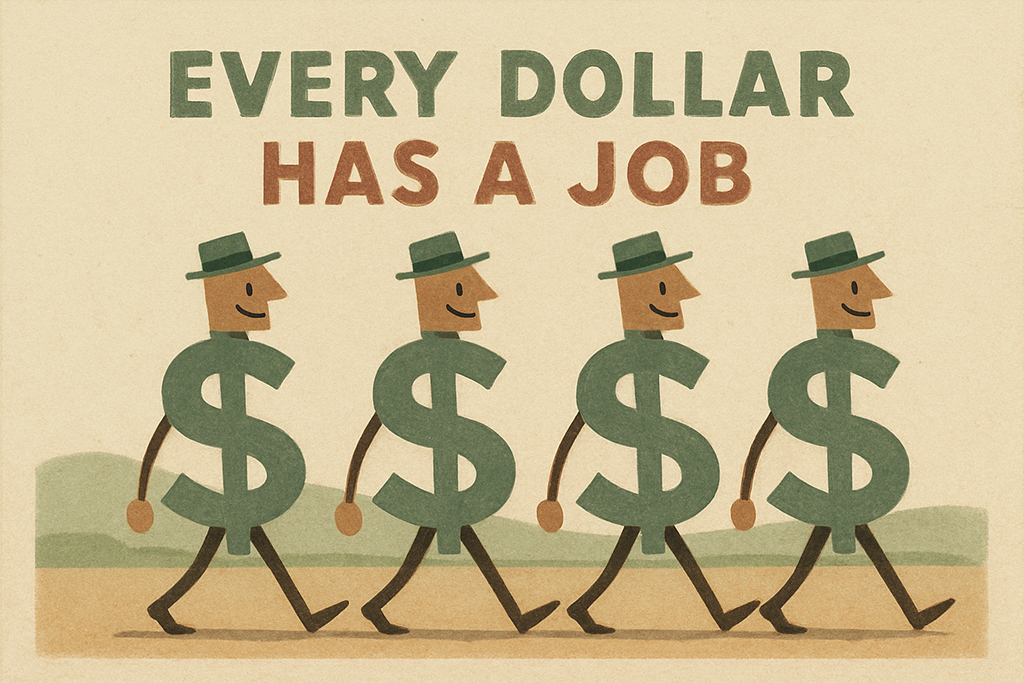

Zero-based budgeting means your income minus your expenses equals zero. Every single dollar gets a job, assignment, or duty. No money sits around waiting to be accidentally spent on things you’ll later regret.

This method started in the corporate world but has become a game-changer for families everywhere. Companies use it to maximize profits, and you can use it to maximize your financial future.

What is Zero-Based Budgeting for Households?

Zero-based budgeting is an intensive budgeting technique where you must justify all expenses from a “zero base” each new period. Think of it as giving your money marching orders every month.

Here’s how it works in simple terms. If you earn $3,000, you allocate all $3,000 for saving, investing, debt payments, or spending. Nothing gets left to chance or impulse purchases.

The “zero” part trips people up sometimes. It doesn’t mean you drain your bank account to $0, so don’t freak out. It simply means you’re assigning a purpose to every dollar you earn.

You can keep a small buffer of $100-$300 in your checking account as a safety net. This cushion helps you avoid overdraft fees and gives you peace of mind. The key is that even this buffer money has a specific job – protecting you from unexpected timing issues with bills.

How to Create Your Zero-Based Budget: A Step-by-Step Guide

Ready to take control? Let’s walk through the exact steps to build your first zero-based budget. Don’t worry – it’s easier than you think.

1. List Your Monthly Income

Start by writing down every source of money coming in. Include your salary, part-time jobs, side hustles, child support, alimony, and even monetary gifts you receive regularly.

Be honest about what you actually bring home after taxes and deductions. Your gross salary looks nice on paper, but your take-home pay is what really matters for your household budget.

If your income changes from month to month, use your lowest monthly earnings from the past year as your baseline. This prevents you from spending money you might not have. When you earn extra, you can always allocate those bonus dollars later.

Variable income can feel scary, but ZBB actually handles it better than traditional budgeting methods. You’re planning for the worst-case scenario while hoping for the best.

2. List All Your Expenses

Time for the detective work. Grab your bank statements and credit card bills from the past three months. You’re about to discover where your money really goes.

Start with your fixed expenses – the bills that stay roughly the same each month. These include rent or mortgage payments, car payments, insurance premiums, and basic utility bills. These are usually easier to predict and plan for.

Next, tackle your variable expenses. These include groceries, dining out, gas for your car, clothing, entertainment, and personal care items. Variable expenses are where most people lose control of their money.

Now comes the fun part – categorizing everything. Sort your expenses into three buckets: needs, wants, and savings/investments. Some financial experts recommend this priority order: saving for emergencies, necessary expenses (food, utilities, housing, transportation, debt payments, long-term savings), and then fun money.

Don’t forget to include savings and debt repayment as expenses. These aren’t afterthoughts – they’re essential parts of your financial plan. Treat them with the same respect you give your rent payment.

3. Assign Jobs to Every Dollar

This is where the magic happens. You’re going to allocate your income to all your categories until your income minus expenses equals exactly zero.

Let’s say you bring home $4,000 per month. You might assign $1,200 for housing, $600 for food, $400 for transportation, $300 for debt payments, $500 for savings, and $1,000 for everything else. Every dollar has a purpose.

If you have money left over after covering all your categories, don’t celebrate yet. Put that extra money to work! Send it toward your emergency fund, throw it at debt, or treat yourself to something special you’ve been wanting. Just make sure it gets assigned to something specific.

What if you’re in the red and your expenses exceed your income? Time to make some tough choices. Look at your “wants” category first – dining out, entertainment, and subscription services are good places to start trimming. You might also need to brainstorm ways to boost your income with a side hustle or selling items you no longer need.

4. Track Your Expenses All Month Long

Here’s where zero-based budgeting separates itself from other methods. You can’t just set it up and forget about it. You need to track every transaction throughout the month.

Some people prefer writing everything down in a notebook. Others love using budgeting apps like EveryDollar or YNAB (You Need A Budget). Cash envelope systems work great for variable spending categories like groceries and entertainment.

When you overspend in one category – and you will at first – you can move money from another category to cover it. Spent $50 more on groceries than planned? Take $50 from your entertainment budget. The key is keeping your overall budget balanced.

This active tracking helps you stay aware of your spending patterns. You’ll start noticing triggers that lead to overspending and develop better financial habits naturally.

5. Adjust and Create a New Budget Every Month

Life changes, and your zero budget should change with it. Plan to review and adjust your budget at least weekly, with a complete refresh every month.

Some months require special planning. December might need extra money for holiday gifts. March might require tax preparation funds. Summer could mean higher air conditioning bills.

The beauty of zero-based budgeting is its flexibility. You’re not locked into rigid categories forever. As your income grows or your priorities shift, your budget can adapt right along with you.

Each month, you’re essentially starting fresh while learning from the previous month’s successes and mistakes. This constant refinement helps you get better at managing money over time.

Advantages of Zero-Based Budgeting for Your Household

Total Financial Control and Intentional Spending

With zero-based budgeting, you know exactly where every dollar is going before you spend it. No more wondering why your checking account is empty or feeling guilty about mystery purchases.

This level of control eliminates financial stress for many people. When you have a plan for every dollar, you can spend money without worry because you know it’s already budgeted for.

Maximizes Efficiency and Optimizes Resource Allocation

Every penny has a specific purpose, ensuring you’re using your money optimally to achieve your financial goals. There’s no waste in a well-executed zero-based budget.

Traditional budgeting often leaves room for money to slip through the cracks. With ZBB, those cracks don’t exist because every dollar is accounted for from day one.

Flexibility and Customization

You set all the rules, and you can adapt your plan monthly based on changes in income, needs, and wants. This makes it more personal than other budgeting methods that use one-size-fits-all approaches.

Your budget should reflect your values and priorities, not some financial guru’s idea of what’s important. Zero-based budgeting gives you that freedom while maintaining structure.

Boosts Savings and Debt Payoff

Saving and debt repayment goals are actively built into your budget from the beginning. You’re not hoping to save whatever’s left over – you’re paying yourself first and making debt elimination a priority.

Many people see dramatic improvements in their savings rate and debt reduction timeline simply because these goals become as important as paying rent or buying groceries.

Forces Financial Reflection

Creating a budget from zero each month encourages mindful spending. You have to review and justify every expense, which helps identify and eliminate unnecessary costs.

How many subscription services are you paying for that you forgot about? Zero-based budgeting forces you to confront these money drains and make conscious decisions about keeping or cutting them.

Great for Beginners

If you’re new to budgeting or feel like you lack control over your money, zero-based budgeting is a fantastic starting point. It helps you get familiar with your accounts, understand your spending habits, and develop financial awareness.

The hands-on nature of this budgeting style accelerates your financial education. You’ll learn more about money management in three months of zero-based budgeting than most people learn in years of casual financial planning.

Potential Challenges and Disadvantages

Time-Consuming and Effort-Intensive

Building a budget from scratch every month and tracking all your expenses requires significant time and effort. Some people find this overwhelming, especially when they’re just starting out.

The good news is that it gets faster with practice. Your first zero-based budget might take several hours to create, but by month three, you’ll probably finish in 30-45 minutes.

Learning Curve and Complexity

The detailed planning can be difficult initially, especially if you have many different financial goals or complex income situations. Don’t expect perfection on your first attempt.

Give yourself permission to make mistakes and learn as you go. Every month will be better than the last as you refine your categories and improve your tracking methods.

Tricky with Unpredictable Income

If your income fluctuates significantly, it can be challenging to allocate funds consistently each month. Freelancers, commission-based workers, and business owners often struggle with this aspect.

Using your lowest income month as a baseline helps manage this challenge. You can always allocate extra money when you have a better month, but you won’t overspend during leaner times.

Risk for “Rebounders”

Some people feel too restricted by detailed budgets and end up rebelling with impulsive overspending.

The key is building in some flexibility and “fun money” categories so you don’t feel completely constrained. A budget should feel empowering, not punishing.

Handling Variable and Unexpected Expenses

Life throws curveballs, and your budget needs to be ready for them. Car repairs, medical bills, and other surprises can derail even the best-planned zero budget.

Create buffer categories for these situations, or build flexibility into your budget by keeping some categories loose enough to absorb unexpected expenses.

Tips for Success with Your Household’s Zero-Based Budget

Stay Honest

Be completely truthful with yourself about your spending habits and income. Your budget only works if it’s based on reality, not wishful thinking.

If you spend $400 per month dining out, don’t budget $100 and hope for the best. Start with your actual spending and gradually reduce it over time if that’s your goal.

Track Everything

Whether you use apps like EveryDollar or YNAB, spreadsheets, or good old pen and paper, find a tracking method that you’ll actually use consistently.

The best tracking system is the one you’ll stick with for months, not the fanciest or most complex option. Simple tools often work better than complicated ones.

Automate What You Can

Set up automatic payments for regular bills, savings transfers, and debt payments. Automation increases your success rate by removing the temptation to skip payments or “borrow” from savings.

Just remember that automation doesn’t mean you can ignore your budget. You still need to track and monitor everything to ensure your automated systems are working correctly.

Create a Buffer Category

Allocate $100-$200 for unexpected expenses in a miscellaneous category. This acts as a small reserve fund within your monthly budget.

This buffer prevents you from blowing up your entire budget when small unexpected expenses pop up. It’s like having a financial shock absorber built right into your plan.

Consistency is Key

Get into a routine of creating and reviewing your budget monthly or bi-weekly. Consistency matters more than perfection, especially when you’re developing this new habit.

Set a specific day each month for budget planning – maybe the last Sunday of the month or the first Saturday. Treat this appointment with yourself as seriously as any other important commitment.

Plan for Irregular Expenses

Set aside money in a separate category for larger, less frequent costs like holiday purchases, car repairs, or annual insurance premiums. These “irregular” expenses are actually quite predictable if you plan for them.

Think through your entire year and identify these larger expenses. Then divide the total amount by 12 and save that amount each month. Your December budget will thank you when holiday spending doesn’t destroy your finances.

Is Zero-Based Budgeting Right for You?

Zero-based budgeting works especially well for certain types of people and situations. You might be a perfect candidate if you want intentional financial planning and to maximize every dollar you earn.

People with variable incomes often love this method because it helps them plan for income fluctuations better than traditional budgeting approaches. If your income varies from month to month, ZBB can provide the structure you need.

Are you looking for a hands-on approach to financial control? Zero-based budgeting requires active participation, which appeals to people who want to be deeply involved in their money management.

New budgeters often find success with this method because it forces them to learn about their spending habits quickly. If you feel like you lack control over your money, this intensive approach can help you regain that control fast.

If you have a steady income and specific financial goals you’re ready to tackle seriously, zero-based budgeting provides the framework to make real progress. Whether you want to pay off debt, save for a house, or build an emergency fund, this method ensures your goals get funded every month.

People who have recently experienced changes in their financial situation – whether due to inflation, job changes, or life events – often benefit from the fresh start that zero-based budgeting provides.

How Zero-Based Budgeting Differs from Traditional Budgeting

Traditional budgeting typically involves making incremental adjustments to previous budgets. You might increase your grocery budget by 5% or add a new category for a gym membership, but the basic structure stays the same.

Zero-based budgeting starts from zero every month, requiring you to justify every expense from scratch. This process can be more efficient at identifying wasteful spending and ensuring your money aligns with your current priorities rather than last year’s habits.

While traditional budgeting can work well for people who want a “set it and forget it” approach, zero-based budgeting is better for those who want maximum control and optimization of their finances.

Think of it as giving your money marching orders every month.

Today is the second-best time to start (the best day was yesterday)

The sooner you get started, the sooner you’ll make progress toward your goals.

Zero-based budgeting empowers you to be completely intentional with your money and make consistent progress toward your financial goals. Instead of wondering where your money went, you’ll know exactly where it’s going before you spend it.

This method isn’t just about tracking expenses – it’s about taking control of your financial destiny. Every dollar becomes a tool for building the life you want instead of just covering whatever seems urgent in the moment.

Consider trying zero-based budgeting for three months to see if it fits your lifestyle and personality. Three months gives you enough time to work through the initial learning curve and experience the benefits.

The first month might feel overwhelming as you figure out your categories and tracking system. The second month will feel more natural as you refine your approach. By the third month, you’ll know whether this budgeting style works for your situation.

Don’t feel like you have to figure everything out alone. Budgeting tools like EveryDollar and YNAB can simplify the process significantly by automating calculations and helping you track expenses throughout the month.

Your financial future depends on the decisions you make today. Zero-based budgeting gives you a proven system for making those decisions with confidence and purpose. Why not start your journey to financial freedom right now?