Is the 20/4/10 Car Rule Your Secret Weapon for Smart Buying?

Buying a car can be exciting. For many people, purchasing a car means freedom or a lifestyle upgrade. But it’s also one of the biggest money decisions you’ll make. How do you make sure you pick the right one without breaking the bank?

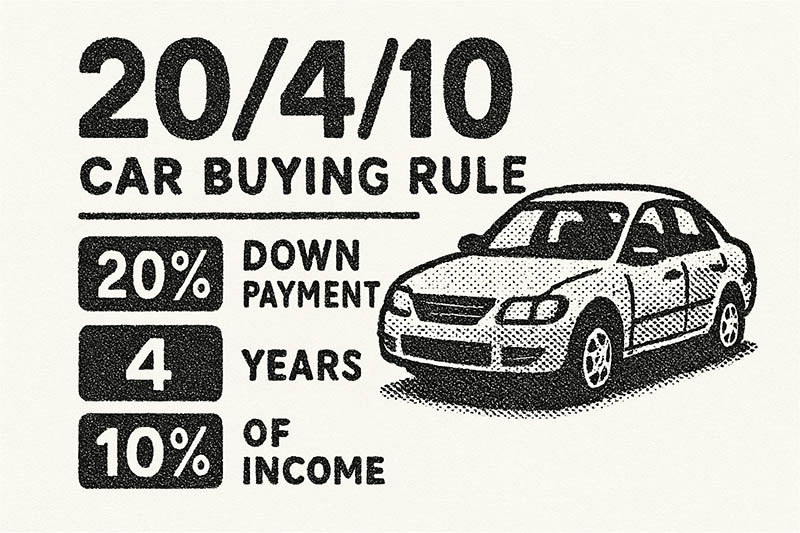

There’s a popular guideline called the 20/4/10 rule that helps people figure out how much car they can truly afford. It’s like a financial roadmap for car buying. This rule looks at three key numbers: your down payment, the loan length, and your total monthly car costs.

But here’s the thing: with new car prices hitting nearly $50,000 and used cars costing an average of $25,512, is this old rule still helpful? Let’s break it down.

Key Takeaways

- The 20/4/10 rule suggests putting 20% down, financing for 4 years or less, and keeping total car costs under 10% of monthly income

- New cars average nearly $50,000 while used cars cost around $25,500 in 2025

- To follow the 10% rule on a $50,000 car, you’d need to earn over $150,000 yearly

- The rule can save you money on interest and help avoid upside-down loans

- It may be unrealistic for many Americans, especially with current car prices and wages

- Consider it as a helpful guide, not a strict law you must follow

Breaking Down the 20/4/10 Rule: What Do the Numbers Mean?

The “20”: Your Down Payment

The rule suggests you pay 20% of the car’s price upfront as a down payment. If a car costs $25,000, you’d aim to put down $5,000. For that $50,000 car? You’d need $10,000 cash. You can run your own numbers using Bankrates Auto Loan Calculator.

A bigger down payment means you borrow less money. This helps you start owning the car faster and lowers your auto loan. It also helps prevent “negative equity” – owing more than the car is worth right away.

Lenders like bigger down payments too. You might get a better interest rate. With excellent credit, you could see rates around 5.25% for new cars, but poor credit could mean paying over 15%.

The “4”: Your Loan Term

The 20/4/10 rule advises taking out a car loan for four years (48 months) or less. Shorter loans mean you pay off the car faster. You’ll usually pay less in total interest too.

It also reduces the risk of the car losing value faster than you pay it off. But here’s the catch: shorter loans mean higher monthly payments. The average new car loan interest rate is 6.73%, while used cars average 11.87%.

While not ideal, a 5 year loan may be easier to fit within your budget. It’s best, however, to stick to a loan term of 4 years or less for used cars which are more than a few years old.

The “10”: Your Total Monthly Car Expenses

All your car-related costs each month should be 10% or less of your monthly income. This isn’t just your car payment! It also covers gas, insurance, and maintenance.

If you make $4,000 a month, your total car costs should be $400 or less. For someone making $70,000 a year, this would be less than $583 per month. You can use your gross income (before taxes) or net income (after taxes), with net income giving you a more careful number.

Keeping car costs low helps you afford other important things. Housing, food, and savings all need their share of your budget too.

The Upside: Why the 20/4/10 Rule is a Smart Move

Saves You Money in the Long Run

With a big down payment and a short loan, you pay much less in interest. Think of it like a discount on the total price of your car!

Let’s say you finance $40,000 at 7% interest. A 4-year loan costs you about $5,800 in interest. A 6-year loan? You’d pay around $8,700 in interest – that’s nearly $3,000 more!

Helps You Stick to Your Budget

This rule gives you clear numbers to work with. It makes it easier to find a car that truly fits your budget. It prevents you from spending too much and helps you keep your monthly cash flow steady.

When you know your limits, you can shop with confidence. No more falling in love with a car you can’t actually afford.

You Own Your Car Faster

A shorter loan term means you get rid of car debt quickly. This frees up your money for other goals sooner. Maybe that’s building an emergency fund or saving for a house.

Plus, you’ll have equity in your car faster. That gives you more options when it’s time to trade up.

Avoids “Upside-Down” Car Loans

A 20% down payment helps you build “equity” from day one. This means you’re less likely to owe more on the car than it’s actually worth.

Cars lose value quickly – especially new ones. New vehicles lose value by nearly 30% over the first two years. Starting with equity helps protect you from this depreciation hit.

Better Loan Offers and Negotiating Power

Lenders often give better interest rates to people who make larger down payments. You’re less risky to them. Knowing your budget also gives you an advantage when talking to car sellers.

You won’t get talked into extras you don’t need. You’ll stick to your plan.

The Downside: Why the 20/4/10 Rule Might Not Always Work

It’s an Older Rule

Some experts say the 20/4/10 rule is outdated. It might have come from the 1970s and hasn’t caught up with today’s economy. Back then, cars were cheaper compared to wages.

The world has changed a lot since then. What worked 50 years ago might not work now.

Cars are Much More Expensive Now

Here’s where things get tough. The average new car costs $49,740 as of late 2024. Used cars average $25,512 in 2025.

But the median household income is around $78,000. To follow the 10% rule for a $50,000 car with good credit, you’d need to make over $150,000 a year. That puts it out of reach for most families.

Car prices have risen much faster than wages. This makes the rule hard for many people to follow.

Monthly Payments Can Be High

A 4-year loan saves interest, but the monthly payments are usually higher than longer loans. This might be tough for some budgets.

Let’s say you finance $30,000 at 7% interest. A 4-year loan means paying about $717 per month. Stretch it to 6 years? Your payment drops to about $510 per month.

Limits Your Car Choices

Sticking strictly to the rule might mean you can’t afford the car you want. This is especially true for new models with all the latest safety features.

Your other bills might also mean you can’t spend the full 10% on transportation. This further limits your options.

Requires a Lot of Cash Upfront

A 20% down payment can be a large amount of money. For a $30,000 car, that’s $6,000 cash. For a $50,000 car? You need $10,000 upfront.

Saving that much cash might delay your purchase. Not everyone has that kind of money sitting around.

Doesn’t Fully Account for Your Credit Score

The rule focuses on percentages, but your credit score is a huge factor here. People with super prime credit (780+) get rates around 5.25%, while those with deep subprime credit face rates over 15%.

A lower credit score means higher interest. You might need an even cheaper car to stay within the 10% rule, even with a big down payment. If you have not checked your credit score lately, now may be a good time. Consider Credit Karma as a valuable resource for this.

Finding Your Balance: Is the 20/4/10 Rule Right for You?

It’s a Guideline, Not a Strict Law

The 20/4/10 rule is a helpful guide, but it’s not a rule you must follow. Everyone’s financial situation is different. What matters most is finding a car you can comfortably afford.

Think of it like GPS directions. It gives you a good route, but you might need to take a detour based on your specific situation.

Tips to Help You Stay Within (or Adjust) Your Budget

Save more for a down payment: If you can, put down more than 20%. This lowers your loan amount and monthly payments. Even 25% or 30% can make a big difference.

Consider a used car: Used cars are often much cheaper than new ones. The average used car costs $25,512 compared to nearly $50,000 for new. This makes it much easier to stick to your budget.

Shop for a base model: Fancy extras add to the price fast. A simpler model can save you thousands. You can always add accessories later if you want.

Boost your credit score: A good credit score gets you better interest rates. Pay your bills on time, keep credit card balances low, and check your credit report for errors.

Compare loan offers and insurance quotes: Don’t take the first offer! Shop around for the best car loan rates. Credit unions often offer the lowest rates. Get insurance quotes before you buy too.

Know your personal budget: Understand how much money you have coming in and going out each month. This helps you see what you can truly afford for transportation costs.

Consider certified pre-owned: These cars offer some warranty protection but cost less than new. They’re often only 2-3 years old with low miles.

Look at total cost of ownership: Factor in gas, insurance, and maintenance costs. A cheaper car that’s expensive to maintain might not be the best deal.

Time your purchase: End of model years, end of months, and end of quarters often have better deals. Dealers want to move inventory.

Get pre-approved: Know your interest rate before you shop. This gives you negotiating power and helps you stick to your budget.

Alternative Rules to Consider

Some experts suggest the 20/3/8 rule instead. That means 20% down, 3 years or less loan term, and 8% of monthly income. It’s even more conservative but might be more realistic for some budgets.

Others focus on the total monthly payment being no more than 15-20% of take-home pay. This includes the loan, insurance, gas, and maintenance.

When to Break the Rule

Sometimes it makes sense to adjust the 20/4/10 rule:

- If you have excellent credit: You might get such a good interest rate that a longer loan makes sense

- If you need a reliable car for work: Your transportation might be an investment in your income

- If you’re buying used: The depreciation hit is already taken, so financing more might be okay

- If you have other debts: You might need to be more conservative with the 10% rule

Making It Work in Today’s Market

With current car prices and interest rates, here are some realistic approaches:

Start with used: Three-year-old used vehicles average over $30,000, but you can find decent cars for much less if you’re flexible on model and features.

Consider financing alternatives: Some credit unions offer better rates than banks or dealer financing. Average rates range from 6.73% for new cars to 11.87% for used cars, but good credit can get you better deals.

Factor in all costs: With gas prices and maintenance costs, make sure you’re accounting for the full cost of car ownership, not just the payment.

Be flexible on the timeline: If saving 20% down will take too long, consider 10-15% down with a slightly longer loan term. The key is finding a balance that works for your specific situation.

The Bottom Line on Car Affordability Rules

The 20/4/10 rule is like a helpful map for car buying. It guides you away from financial trouble. But just like a map, you might need to adjust it for your own journey and today’s changing car market.

The most important thing is that you know what you can comfortably afford. Don’t let a car payment stress you out or keep you from reaching other financial goals.

With new car prices near $50,000 and median household income around $78,000, the traditional rule might not work for everyone. But the principles behind it – don’t borrow too much, pay it off quickly, and keep total transportation costs reasonable – are still smart.

Whether you follow the 20/4/10 rule exactly or create your own version, the goal is the same: get reliable transportation without breaking your budget. Your future self will thank you for making a smart choice today.

Remember: the best car buying rule is the one that helps you sleep well at night, knowing you made a decision you can afford.